With the ARIMA procedure, you can create an autoregressive integrated moving-average (ARIMA) model that is suitable for finely tuned modeling of time series.

ARIMA models provide more sophisticated methods for modeling trend and seasonal components than do exponential smoothing models, and they have the added benefit of being able to include predictor variables in the model.

Continuing the example of the catalog company that wants to develop a forecasting model, we have seen how the company has collected data on monthly sales of men's clothing along with several series that might be used to explain some of the variation in sales. Possible predictors include the number of catalogs mailed and the number of pages in the catalog, the number of phone lines open for ordering, the amount spent on print advertising, and the number of customer service representatives.

Are any of these predictors useful for forecasting? Is a model with predictors really better than one without? Using the ARIMA procedure, we can create a forecasting model with predictors, and see if there's a significant difference in predictive ability over the exponential smoothing model with no predictors.

With the ARIMA method, you can fine-tune the model by specifying orders of autoregression, differencing, and moving average, as well as seasonal counterparts to these components. Determining the best values for these components manually can be a time-consuming process involving a good deal of trial and error so, for this example, we'll let the Expert Modeler choose an ARIMA model for us.

We'll try to build a better model by treating some of the other variables in the dataset as

predictor variables. The ones that seem most useful to include as predictors are the number of

catalogs mailed (mail), the number of pages in the catalog (page),

the number of phone lines open for ordering (phone), the amount spent on print

advertising (print), and the number of customer service representatives

(service).

- Double-click the Type node to open its properties.

- Set the role for

mail,page,phone,print, andserviceto Input. - Ensure that the role for

menis set to Target and that all the remaining fields are set to None. - Click Save.

- Double-click the Time Series node.

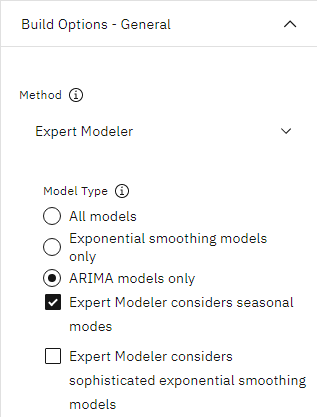

- Under BUILD OPTIONS - GENERAL, select Expert Modeler for the method.

- Select the options ARIMA models only and Expert Modeler

considers seasonal models.

Figure 1. Choosing only ARIMA models

- Click Save and run the flow.

- Right-click the model nugget and select View Model. Click

men and then click Model information. Notice how the

Expert Modeler has chosen only two of the five specified predictors as being significant to the

model.

Figure 2. Expert Modeler chooses two predictors

- Open the latest chart output.

Figure 3. ARIMA model with predictors specified

This model improves on the previous one by capturing the large downward spike as well, making it the best fit so far.

We could try refining the model even further, but any improvements from this point on are likely to be minimal. We've established that the ARIMA model with predictors is preferable, so let's use the model we have just built. For the purposes of this example, we'll forecast sales for the coming year.

- Double-click the Time Series node.

- Under MODEL OPTIONS, select the option Extend records into the future and set its value to 12.

- Select the Compute future values of inputs option.

- Click Save and run the flow.The forecast looks good. As expected, there's a return to normal sales levels following the December peak, and a steady upward trend in the second half of the year, with sales in general better than those for the previous year.

Figure 4. Sales forecast extended by 12 months